Madrid, 25th July 2019

Highlights:

- Leader in fibre, both in Europe and Latin America. Telefónica’s FTTx/cable coverage exceeded 121 million premises passed, the largest network outside China. Of the total, 53 million passed through our own fibre network.

- Higher value, more satisfied and more loyal customers. Average revenue per user (ARPU) increased 4.4% and churn remains stable.

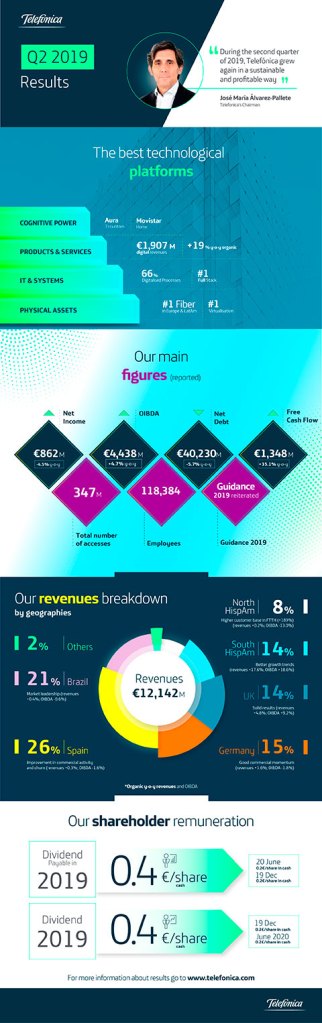

- Revenues: profitable and sustainable growth. Revenues for the April-June period increased 3.7% year-on-year, with all regions growing organically in the semester. In reported terms, revenues stabilized in the quarter for the first time in eight quarters. Broadband & services over connectivity already account for 55% of total revenues and are increasingly less exposed to regulation. OIBDA was up 1.6%, both in organic terms.

- Advances in our transformation thanks to a more efficient use of networks and end-to-end digitalization. Telefonica has reached network sharing agreements in Germany, Brazil and UK, which will generate efficiencies and allow faster roll-outs. We are on track to deliver the digital transformation plan in terms of savings, with 45% of the objective already achieved at the end of June.

- Debt reduction for the 9th consecutive quarter. Net debt fell by 5.7% year-on-year and stood at 40,230 million euros at June 30, mainly due to free cash flow generation (2,756 million euros in the semester). Including asset sales already announced, net debt decreased by approximately € 1,500M, to € 38,700M.

José María Álvarez-Pallete, Chairman and Chief Executive Officer:

“We have demonstrated the consistency of our transformation strategy towards a technology company, backed by our results. We are back to a sustainable and profitable growth. Our accesses were up, especially in the high-value segments, while average revenue per access increased (+4.4% y-o-y) and churn rate remained stable. This shows that our commercial strategy is bearing fruits, underpinned by increasingly advanced networks that allow us to better service our customers’ needs. This turns into increased customer satisfaction rate, which makes this strategy even more sustainable.

Organic growth trends (revenues +3.7% and OIBDA +1.6% y-o-y) are consistent with this year’s targets, which we reiterate. Growth is profitable and driven by the digitalisation and simplification plan, among other measures.

This profitable and sustainable growth has further allowed us to reduce debt, which comes down for the ninth consecutive quarter, thanks to healthy cash generation (+78.0% in the first half of the year)”.

Financial results January-June 2019:

Telefónica today presented its financial results for the first half of 2019. The figures showed the profitable and sustainable growth of main indicators, as well as a strong cash generation and a further debt reduction, for the ninth consecutive quarter, reinforcing the financial position of the company.

Higher customer value

Telefónica Group’s access base stood at 346.6m at June 2019, and improved in value, with average revenue per access growing to +4.4% y-o-y organic, while churn remained stable, thanks to the strategic focus on value customers, which continued posting solid growth.

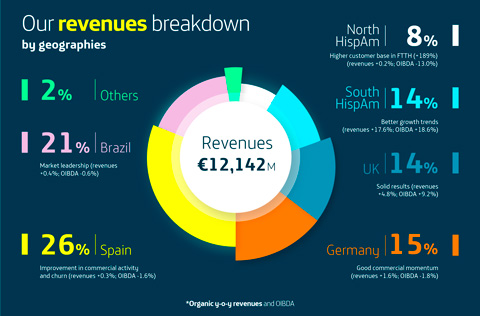

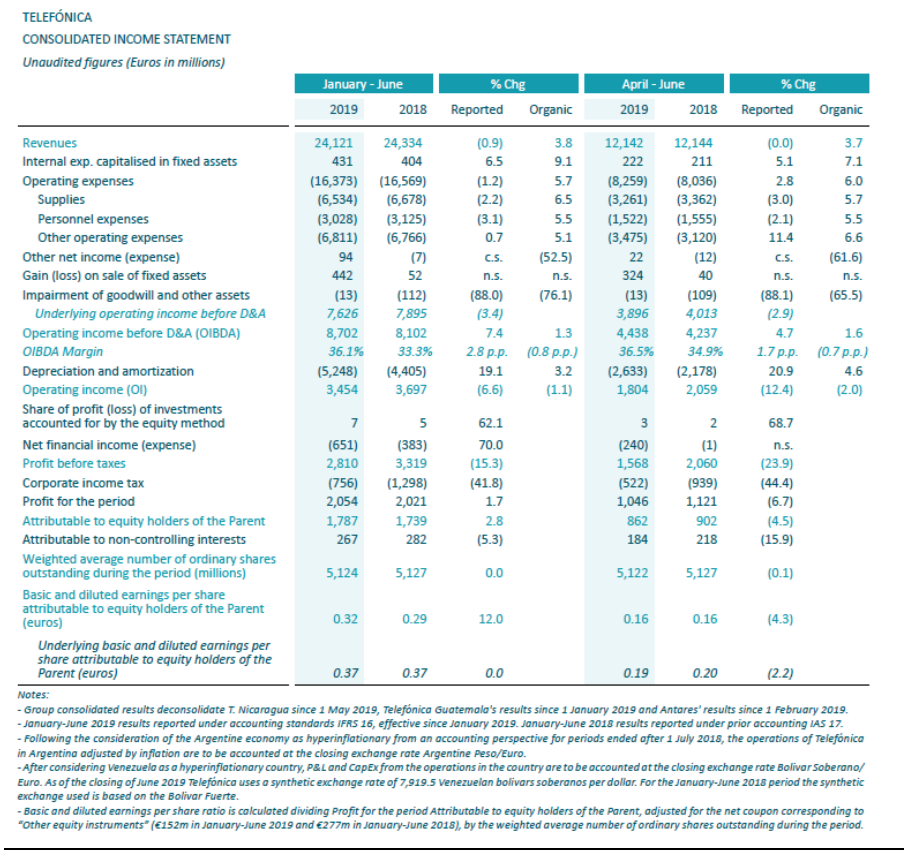

Revenues totalled €12,142m in the second quarter and grew 3.7% y-o-y organic (€24,121m in January-June, +3.8%) and remained stable y-o-y in reported terms. The growth in the quarter came from the solid growth in service revenues (+2.3%) and the strong advance of handset sales (+16.7%). Excluding the negative impact from regulation (-0.6 p.p. in the second quarter; -0.7 p.p. in the first half) revenues would have grown by +4.3% y-o-y organic (+4.5% in January-June).

Revenues coming from broadband and services beyond connectivity accounted for 55% of the total in the second quarter (+2 p.p. y-o-y), reflecting the Company’s focus on data monetization and digital services, as well as a further advance in the transformation process. Digital service revenues reached €1,907m in April-June (+19.0% y-o-y) and €3,783m in the first half of the year (+20.1% y-o-y).

Operating expenses (€8,259m in April-June; +2.8%; €16,373m in January-June, -1.2%), were affected by the positive impact recorded in the second quarter of 2018 associated with a favourable court ruling in Brazil (€485m), which more than offset the positive impact in 2019 associated with the application of the new IFRS 16 accounting standard mentioned above.

It is important to highlight the reported variation of the consolidated financial statements for the first half 2019 reflected the adoption of IFRS 16 since 1 January 2019 (the statements for January-June 2018 were reported according to IAS 17). The organic variation excludes the impact of the accounting change to IFRS 16 (+€354m in April-June and +€768m in January-June on OIBDA; and -€70m and -€87m on the net income). The Consolidated Statement of Financial Position at 30 June 2019 includes lease liabilities, including those held for sale, amounting to €7,542m.

The evolution of exchange rates negatively affected the Company’s reported results mainly due to the depreciation of the Brazilian real and the Argentine peso against the Euro, although the trend improved sequentially. In the second quarter of 2019 foreign currencies reduced y-o-y revenue growth by 4.1 p.p. and OIBDA by 3.6 p.p. However, the negative impact of the depreciation of currencies at the OIBDA level (-€332m in the first half) decreased significantly in terms of cash flow generation (-€91m). The results were also affected by the exit from the perimeter of consolidation of T. Nicaragua (since 1 May 2019), T. Guatemala (since 1 January 2019), and Antares (since 1 February 2019).

OIBDA (€4,438m in April-June; €8,702m in January-June) increased by 4.7% y-o-y in the second quarter (+1.6% organic) and by +7.4% in the first half of the year (+1.3% organic), positively affected by the impact of the new IFRS 16 accounting standard. Excluding the negative impact of regulation (-0.6 p.p. in April-June; -0.6 p.p. in January-June), OIBDA would have increased by 2.2%% y-o-y organic (+1.9% in the first half).

OIBDA margin stood at 36.5% in the second quarter, expanding 1.7 p.p. y-o-y (-0.7 p.p. organic). In January-June, OIBDA margin expanded by 2.8 p.p. y-o-y to 36.1%.

Net income in January-June reached €1,787m (+2.8%). In April-June, it stood at €862m and decreased 4.5% y-o-y affected by the following impacts: i)provision for tax litigations (-€152m); ii) hyperinflation adjustment in Argentina (-€101m); iii) depreciation and amortisation charges arising from purchase price allocation processes (-€93m); iv) adoption of IFRS 16 accounting standard (-€70m) and iv) restructuring costs (-€14m). In positive: i) interests associated to the extraordinary tax refund in Spain (+€151m) ii) net capital gains from the sale of companies (+€62m) and ii) the growth of T. Venezuela (+€37m). Basic earnings per share amounted to €0.32 and increased by 12.0% in the first half of the year (€0.16 in the second quarter; -4,3% interanual).

CapEx in January-June totalled €3,385m (-13.9% y-o-y) and included €22m of spectrum (€4m in the second quarter mainly in T. Argentina). In organic terms, it increased 6.3% y-o-y affected by a different calendar of execution, decelerating its growth trend in the second quarter (+2.4%), and continued to focus on accelerating excellent connectivity (deployment of LTE and fibre networks, increased network capacity and virtualisation) and improving quality and customer experience (implementation of AI in the Company’s technology platforms).

Operating cash flow (OIBDA-CapEx) reached €5,317m in the first half of 2019, up 27.5% y-o-y (-2.4% organic, affected by a different calendar of CapEx execution). Operating cash flow boosted 45.1% y-o-y in the second quarter (+0.9% organic).

Free cash flow before principal payments of lease liabilities reached €3,587m in January-June 2019. However, after these payments (-€831m), free cash flow totalled €2,756m in January-June 2019 and increased by 78.0% y-o-y.

Definition: Assumes average constant foreign exchange rates of 2018, except for Venezuela (2018 and 2019 results converted at the closing synthetic exchange rate for each period) and excludes the hyperinflation adjustment in Argentina. Considers a constant perimeter of consolidation. Excludes the effect of the accounting change to IFRS 16, write-downs, capital gains/losses from the sale of companies, restructuring costs and material non-recurring impacts. CapEx excludes spectrum investments.

Debt reduction for the 9th consecutive quarter

Net financial debt decreased 5.7% y-o-y and stood at €40,230m at the end of June. Against December 2018, net debt decreased by €844m thanks to free cash flow generation (€2,756m) and net financial divestments mainly from the sale of T. Nicaragua, T. Guatemala and Antares (€321m). In contrast, the factors that increased debt were: i) shareholder remuneration (€1,089m, including the replacement of capital instruments and coupon payments), ii) labour-related commitments (€419m) and iii) other factors for a net amount of €726m.). Including asset sales already announced, net debt decreased by approximately € 1,500M, to € 38,700M.

In the second quarter, net financial debt decreased by €151m thanks to free cash flow generation (€1,347m) and net financial divestments mainly from the sale of T. Nicaragua (€182m). On the other hand, following the adoption of IFRS 16, lease liabilities, including those held for sale, amounted to €7,542m. Net financial debt including lease liabilities was €47,772m.

In January-June 2019, the financing activity of Telefónica amounted to approximately €5,699m equivalent (without considering the refinancing of commercial paper and short-term bank loans) and focused on maintaining a solid liquidity position and refinancing and extending debt maturities (in an environment of low interest rates). Therefore, as of the end of June, the Group has covered debt maturities for the next two years. The average debt life stood at 10.3 years (vs. 9.0 years in December 2018).

Advanced networks and excellent connectivity

Telefónica, through excellent connectivity, continues with its digital transformation towards a technology company. Smart connectivity over new, highly available and fast networks, which are flexible, secure and advanced, and integrate elements of artificial intelligence guaranteeing accessibility to the latest generation services that customers are demanding. Commercial operations in the online channel accelerated and grew by 28% y-o-y in January-June and 12% y-o-y reduction in calls handled in the first half of the year.

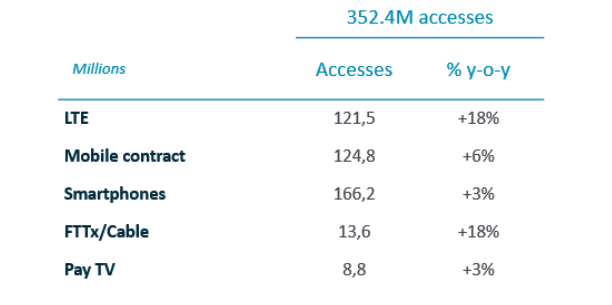

The Group’s FTTx/cable coverage reached 121m of premises passed (53.2m in own network; +12% y-o-y; 22.2m FTTH in Spain, 20.3m in Brazil and 10.6m FTTx/cable in HispAm, +29% y-o-y. Deployment in Latin America benefits from an already industrialised process, and both lower deployment (-50% in the last 5 years in Spain) and maintenance costs (failure rate 50% lower than copper in Spain and Brazil). Retail fibre and cable accesses connected amounted to 13.9m (+14% y-o-y), where UBB accounted for 65% of total broadband accesses (+8 p.p. y-o-y); and in Spain wholesale fibre accesses amounted to 1.9m (+61% y-o-y), increasing the return on investment. In LTE coverage reached 78% (4 p.p. y-o-y; 95% in Europe and 73% in Latin America) and traffic accounts for 73% of the total. Besides, Telefonica has reached network sharing agreements in Germany, Brazil and UK, which will generate efficiencies and will allow faster roll-outs.

The E2E Digital Transformation programme is focused on offering a more digital customer experience, facilitating the launch of services and making the cost structure more flexible. Out of the 2019 savings target, 45% was reached in January-June, in line with expectations (>€340m in addition to the more than €300m achieved in 2018).

Results by geographies:

(% organic y-o-y)

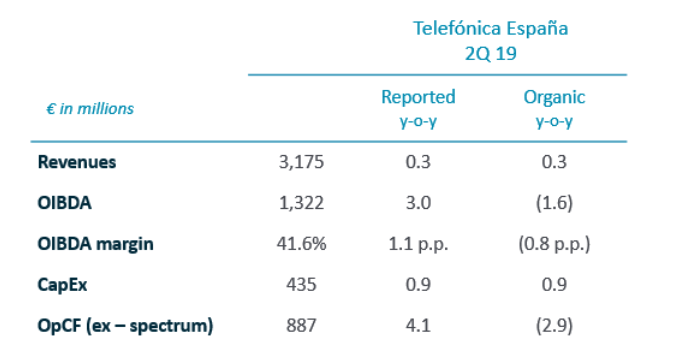

Telefónica España: a differentiated positioning improved commercial activity, and service revenue grew for 8th consecutive quarter. Service revenues at Telefónica España grew for the eighth consecutive quarter (+0.3% y-o-y in the second quarter), thanks to the Company’s differentiated positioning and the improvement in the commercial activity in all segments, especially in higher value accesses.

Revenues in the quarter totalled €3,175m, growing 0.3% y-o-y, in line with the previous quarter, thanks to the growth in service revenues (€3,086m; +0.3% y-o-y) and handset revenues (+0.5% y-o-y). In the first half, revenues stood at €6,283m (+0.3% y-o-y) and service revenues amounted to €6,119m (+0.5% y-o-y).

OIBDA in April-June totalled €1,322m, posting a 3.0% y-o-y reported growth impacted by i) factors mainly related to real estate sales (+€32m) and ii) changes from the adoption of IFRS 16 (+€59m). In January-June, OIBDA amounted to €2,672m, +6.6% reported impacted by i) changes due to the adoption of IFRS 16 (+€123m), ii) factors mainly related to real estate sales in the second quarter (+€32m), iii) capital gain from the assignment of future rights in the first quarter (+€103m) and iv) provision for the restructuring of channels in the first quarter (-€23m). In organic terms, OIBDA fell 1.6% y-o-y (-1.5% in the first half of the year), mainly due to higher growth in supply costs. OIBDA margin stood at 41.6% (-0.8 p.p. y-o-y) and at 42.5% in the quarter (-0.7 p.p. y-o-y).

CapEx in the first half of the year (€813m) rose 4.6% y-o-y (+0.9% in the quarter), growth that will continue to slow throughout the year. Operating cash flow amounted to €1,859m.

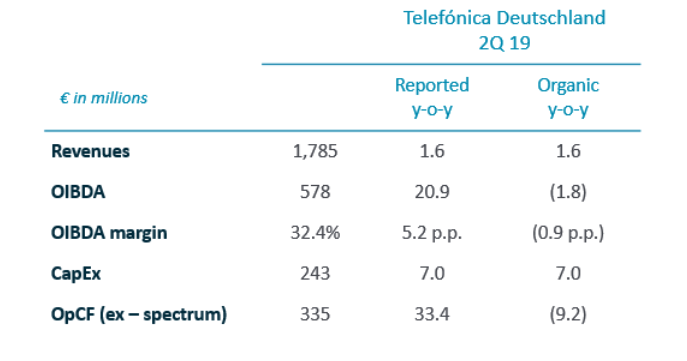

Telefónica Deutschland: good commercial momentum and revenue acceleration up to 1.6%. Telefónica Deutschland continued with its transformation and market investment delivering another quarter with strong trading and operational momentum in both, own and partner brands, in a dynamic while rational market environment. The O2 Free portfolio together with the newly launched value-added services O2 TV and O2 Cloud continued to be well received and drove further data usage and ARPU uplift.

Revenues accelerated growth to +1.6% y-o-y in Q2 19 (+0.7% in Q1) and reached €1,785m (€3,564m in H1 19; +1.1% y-o-y) due to solid MSR performance and ongoing strong demand for handsets.

OIBDA reached €578m in Q2 19, down 1.8% y-o-y (€1,101m; -1.1% in H1) mainly due to the combination of the ongoing transformation and market investment to drive future growth, regulatory impacts of -€10m in Q2 (-€15m in H1; mainly MTR cuts, intra-EU calling, RLAH), remaining network synergies (+€10m in Q2; +€30m in H1) and early transformation benefits of +€10m in Q2 (+€15m in H1). OIBDA margin decreased by -0.9 p.p. y-o-y in the quarter (-0.6 p.p. in H1).

CapEx reached €496m in H1 19 and increased by +16.9% y-o-y, including synergies of €25m (€10m in Q2). This was mainly due to front-loaded LTE roll-out investment in suburban areas and network densification (~4,400 sites added by end of June) with a clear focus on improving customer experience, a trend expected to normalise over the year. As such, operating cash flow (OIBDA-CapEx) stood at €605m in the period January to June 2019.

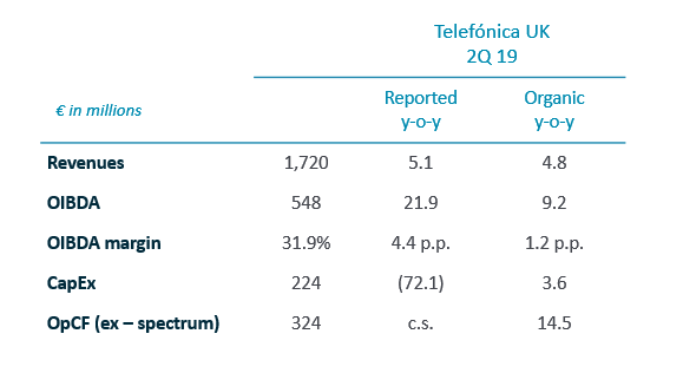

Telefónica UK: solid quaterly results, with revenue growth (+4, 8%). Telefónica UK delivered another robust set of results in the second quarter, posting healthy top-line, operating cash flow and customer growth in a competitive market. The Company demonstrated once again its market leading position and remained UK’s favourite mobile network with continued sector leading loyalty at 0.9%, supported by the success of innovative customer propositions such as “Custom Plans”, which gives customers control and flexibility.

Revenues (€1,720m) maintained solid growth of 4.8% y-o-y in Q2 19 (€3,411m; +5.1% in H1). This top-line growth was mainly driven by strong demand for higher value handsets supported by the success of the flexible “Custom Plans”, continued growth in the Smart Metering Implementation Programme (SMIP) as well as MVNO revenues. OIBDA totalled €548m in Q2 19 and strongly grew by 9.2% y-o-y (€1,052m; +6.4% in H1). This robust y-o-y performance was mainly supported by the ongoing solid revenue trends and efficient cost management, along with a net positive effect of €23m related to special factors. IFRS 16 accounting changes accounted for a positive impact of €55m in Q2 (€110m in H1). OIBDA margin increased by 1.2 p.p. y-o-y in Q2 (+0.3 p.p. in H1).

CapEx amounted to €409m, up 2.0% y-o-y in H1 19 and reflects continued investment in network capacity and customer experience. Operating cash flow (OIBDA-CapEx) increased by 10.0% y-o-y in the first half of the year.

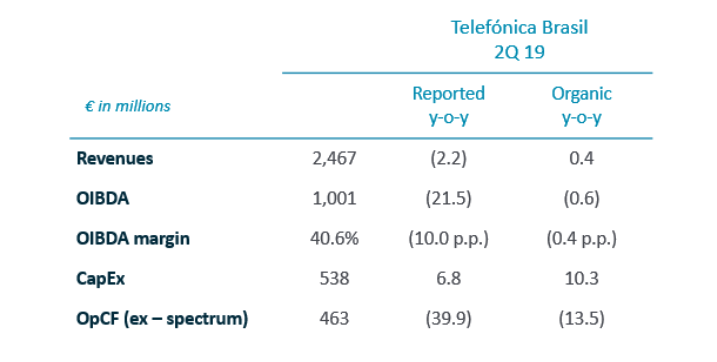

Telefónica Brasil: sustained market leadership and improved commercial activity in mobile contract, fibre and IPTV. Telefónica Brasil maintained its strategy of creating sustainable value. The growth in mobile contract and fibre accesses, coupled with the efficiencies associated with the digitalisation process, translated into a 40.8% OIBDA margin and a 12.7% annual increase in Free Cash Flow (under Telefonica Brasil reporting criteria) in the first half of the year.

Revenues in the quarter (€2,467m) continued posting y-o-y growth (+0.4%; 5,030m, +1.1% in the first half) thanks to mobile service revenues and handset sales (+31.9% vs. +42.3% in the first half).

OIBDA amounted to €1,001m (impacted by €108m resulting from changes arising from the adoption of IFRS 16, €214m in H1) and fell by 0.6% in the quarter (€2,050m, +1.2% in the first half). OIBDA margin in the quarter was 40.6% (-0.4 p.p. y-o-y; 40.8% in the first half, stable y-o-y).

CapEx in the first half of the year amounted to €934m (+10.0% y-o-y), mainly allocated to FTTH deployment (21 new cities deployed in H1) and the expansion of the 4G network to 3,166 cities (88% of the population; +2 p.p. y-o-y). Capex in the quarter accounted for 19% of revenues (+2 p.p. y-o-y). Operating cash flow amounted to €1,117m in the first half of the year, down 6.6% due to the higher investment effort above mentioned.

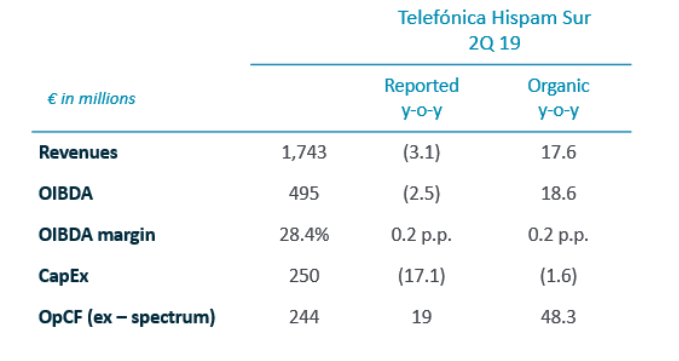

Telefónica Hispam Sur: improved trends in revenue and OIBDA. Hispam Sur’s second quarter results showed improved trends in revenue (+17.6% y-o-y vs. +15.2% in 1Q, mainly due to better mobile service revenues in Argentina and Peru) and OIBDA growth (+18.6% vs. +7.0% in Q1, with growth in all the countries of the region). These good results are underpinned by the better quality of the customer base (higher penetration of contract accesses, FTTx and Pay TV) by the progressive tariff update in Argentina and the continued digitalisation process.

Revenues for April-June amounted to €1,743m, up 17.6% y-o-y (+16.4% in the first half of the year) due to mobile service revenues, +17.8% y-o-y (+16.5% in January-June), and it is worth highlighting: i) the improvement seen in Peru (+0.8 p.p. vs. Q1 y-o-y), due to the tariffs update in the fixed business and the good performance of the convergent product and ii) the acceleration in Argentina. Handset revenues maintained a strong pace of growth at +16.0% (+15.8% in the first half).

OIBDA (€495m in Q2; positively impacted by €19m as a result of changes arising from the adoption of IFRS 16, €58m in H1) grew 18.6% y-o-y in the quarter (+12.7% in the first half), showing improved performance mainly in Argentina and Peru. OIBDA margin was 28.4% (+0.2 p.p. y-o-y; 27.9% in H1, -0.9 p.p. y-o-y).

CapEx amounted to €493m in H1 (+14.2% y-o-y), mainly allocated to the deployment of the 4G network and FTTx and cable networks. CapEx accounted for 15% of revenues in H1 (stable y-o-y). Operating cash flow (OIBDA-CapEx) totalled €443m in the first half (+11.0% y-o-y).

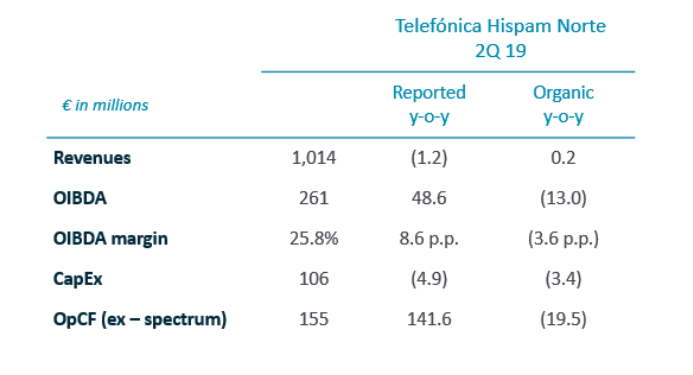

Telefónica Hispam Norte: growth in the high-value segments. Hispam Norte presented positive commercial results in the second quarter of 2019, with growth in the high-value segments: contract and LTE accesses in mobile, and FTTH in fixed.

Revenues (€1,014m) increased 0.2% y-o-y in the quarter (€1,985m, +0.7% in H1). OIBDA (€261m positively impacted by €35m as a consequence of changes following IFRS 16 adoption; +€79m in H1) fell 13.0% y-o-y in the quarter (€525m in H1, -13.9%), still strongly affected by the spectrum commitments in Mexico previously mentioned, and partially offset by the growth seen in Colombia and Central America (+11.6% y +13.1%, respectively). OIBDA included €33m capital gain from the sale of towers (€9m capital gain from the sale of real estate and €14m from the sale of fibre in Q2 18). OIBDA margin stood at 25.8% (-3.6 p.p. y-o-y; 26.4% in H1, -4.0 p.p.).

CapEx (€184m in January-June) increased 3.2% y-o-y and was mainly allocated for expanding LTE and fibre networks. CapEx (excluding spectrum) accounted for 8% of total revenues in H1 (-0.7 p.p. y-o-y). Operating cash flow (OIBDA-CapEx) totalled €340m in the first half (-21.4% y-o-y).

Further significant information

pr-Q2-2019-telefonica-results.pdf