Madrid, 20th February 2020

The company starts 2020 advancing on the execution of its new strategy, focused on creating long term value

Highlights:

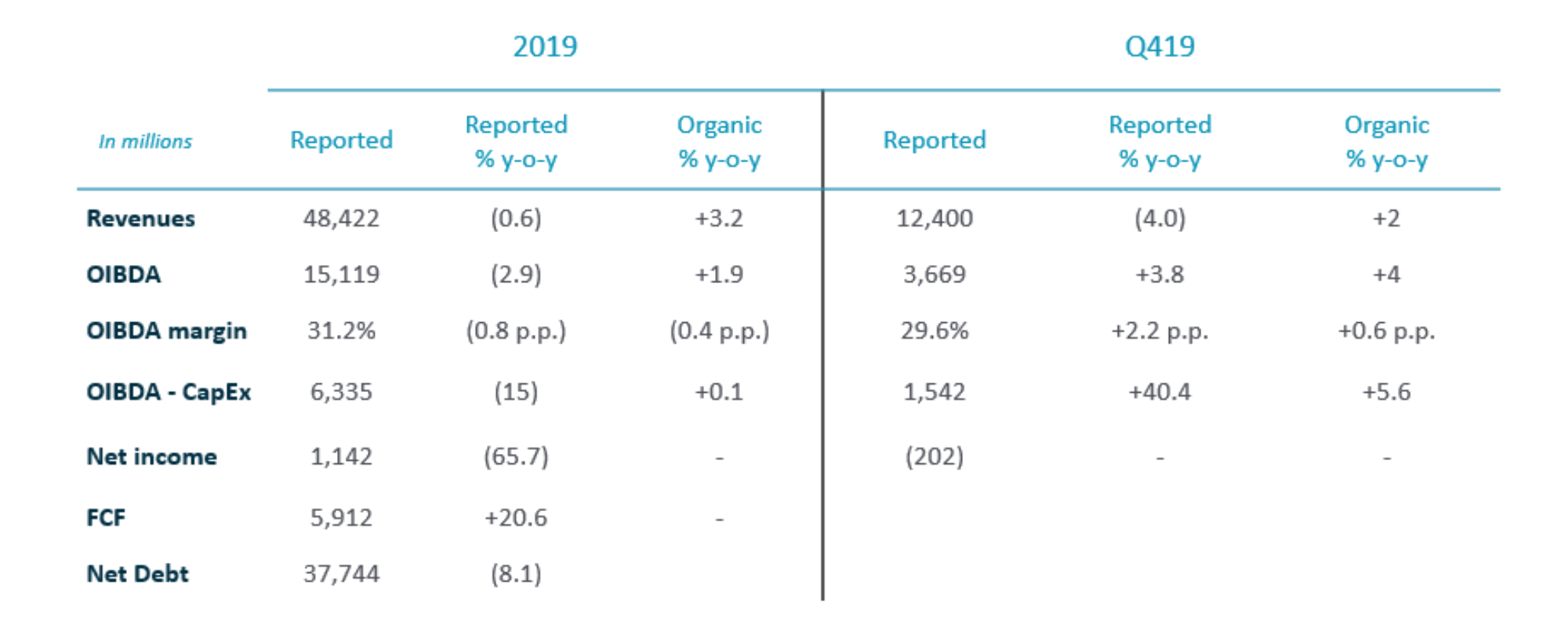

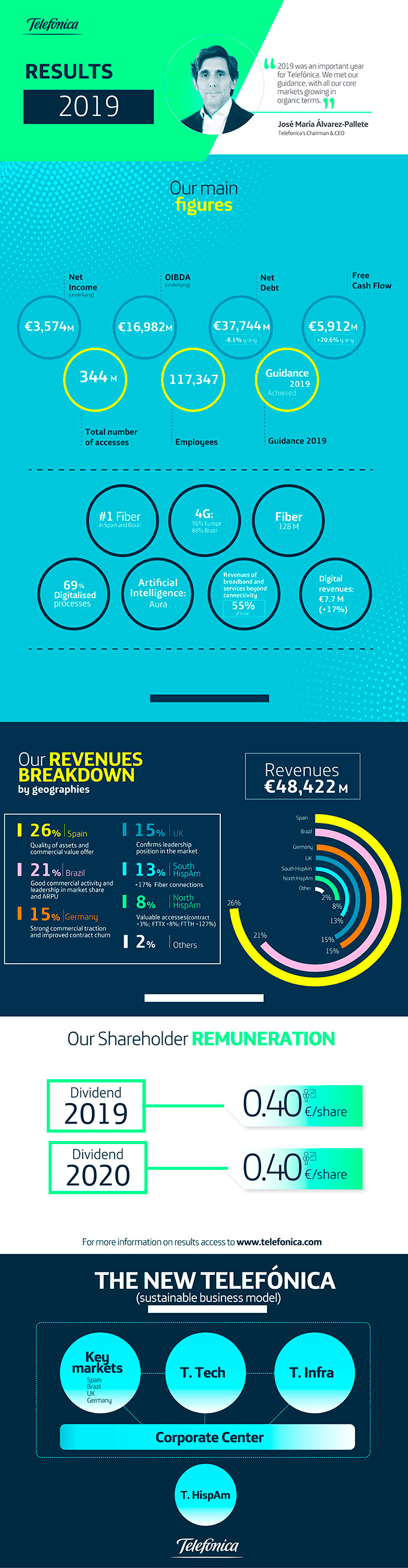

- Sustainable growth: Telefónica revenues grew in organic terms for the sixth consecutive year, up +3.2% to 48,422M€ (-0.6% reported), mainly due to the sustained revenue growth in its main markets. Digital service revenues grew 17.1% in 2019.

- Profitable growth: OIBDA grew +1.9% in 2019 in organic terms (€15,119M, -2.9% reported), backed by revenue growth and efficiencies from digitalisation and simplification. Telefonica captured more than €420m in digital transformation savings in 2019 and reached two-thirds of the €1bn target committed for the 2017-2020 period.

- Responsible growth: Telefónica reported a stable accesses base of 344 million and improved customer satisfaction, which translated into an improvement in ARPU of 4.3% and a stable churn.

- Net income, excluding extraordinary impacts of €2,432m, reached €3,574M (€1,142M in reported terms). The main impact comes from a €1,614m provision from restructuring expenses, mainly in Spain.

- Free Cash Flow grew 20.6% up to €5,912M, reaching the highest level since 2013.

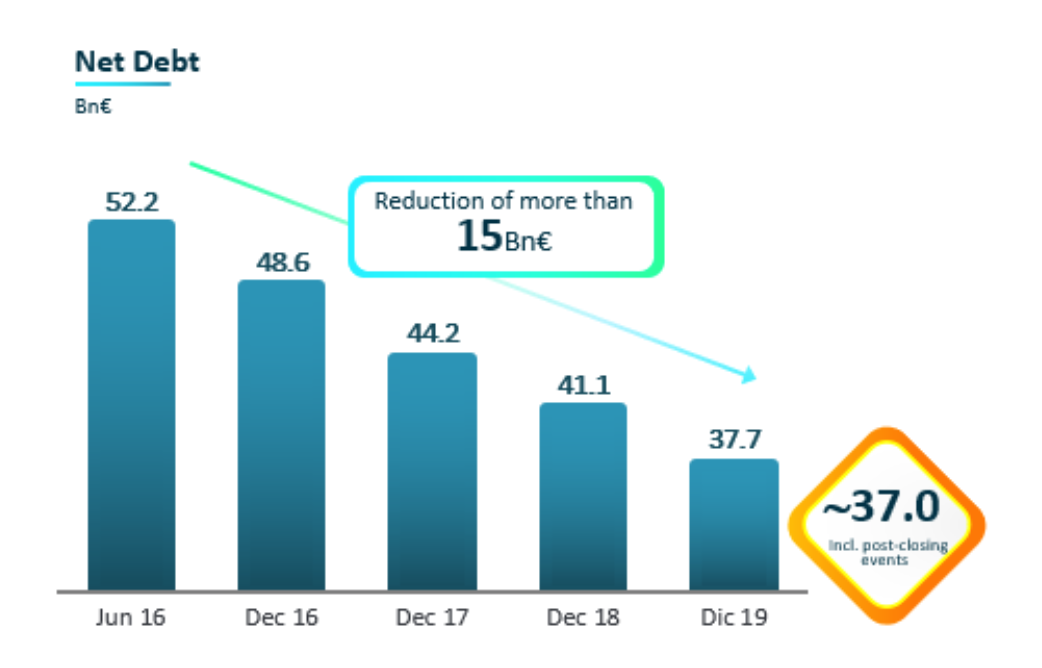

- Net debt reduction for the 11th consecutive quarter, €37,744M, 8.1% below the level at December 2018, and close to €15,000M below June 2016. Including post-closing events, debt would be approximately €37,000M.

Guidance and shareholder remuneration:

- The Company confirms shareholder remuneration for 2019 and announces the remuneration policy for 2020, a dividend of €0.40 per share, to be paid in December 2020 (€0.20 per share) and in June 2021 (€0.20 per share)1.

- Telefónica met 2019 financial guidance and announces new guidance for 20202 of stable revenues, OIBDA and OIBDA-CapEx to revenues

- Telefónica announces financial guidance for 2019-20222 related to the action plan presented in November 2019:

- Revenue growth.

- More than €2,000M of additional revenues in Telefonica Tech (Cloud, IoT/Big Data and Cibersecurity) in 2022.

- 2 p.p. increase in OIBDA-Capex to revenues by 2022.

1 The adoption of the corresponding corporate resolutions will be proposed in due course, announcing the specific payment dates.

2 2020 and 2019-2022 guidance:

Assumes constant exchange rates of 2019 (average in 2019). – Exclude the contribution to growth from T. Argentina and T. Venezuela. -Exclude the results from Central America’s operations. -Considers constant perimeter of consolidation. /- Does not include write-offs, capital gains/losses from the sale of companies, material non-recurring impacts and restructuring costs. – CapEx excludes investments in spectrum. -2019 adjusted bases: Revenues (€47,875m), OIBDA (€16,762m), and (OIBDA-CapEx)/Revenues (19.9%). -Considering: average exchange rates in 2019 with the exception of Venezuela and Argentina (exchange rate of the end of the period). – Excludes T. Centroamérica. IFRS 16.

José María Álvarez-Pallete, Chairman and Chief Executive Officer:

“2019 was an important year for Telefónica. We met our guidance, with all our core markets growing in organic terms. We are becoming more efficient based on digitalisation and shutting down legacy services. We delivered very strong free cashflow in 2019, leading to a continued reduction in debt for 11 consecutive quarters, also helped by disposals and other actions to improve return on capital employed. We continue to invest in next generation networks, cementing our leadership in fibre networks in both Europe and Latin America. Thanks to years of investment, our CapEx to sales ratio peak is behind us.

We are also making good progress in achieving non-financial objectives, including an improvement in both customer and employee satisfaction. Our staff and board are more diverse. We are aware that our sector has a great impact on the societies where we operate. Our digital customer solutions, as well as energy efficient networks, are helping to decarbonize the economy. Last year we reduced CO2 emissions by 18%, reaching a 50% reduction in four years.

We begin 2020 with good momentum and focus on executing the plan we announced at the end of last year. Telefónica took five strategic decisions to generate value and long-term positive impact to all stakeholders. We are prioritising markets where we can be relevant for our customers – Spain, Brazil, Germany and the UK – while focusing on value creation in new digital services and infrastructure through T. Tech and T. Infra. The operational spin-off of Hispam will open opportunities to crystallise value and finally, we are increasing agility and efficiency across all units.

Looking to our 2020 guidance, we are expecting stable growth in the main metrics, a stable and attractive dividend, with a long-term commitment to a sustainable and responsible growth.”

Financial results January-December 2019:

Telefónica Group’s access base stood at 344.3m at December 2019 and remained virtually stable y-o-y excluding changes in the perimeter. Customer value continued to improve with an average revenue per access increase of 3.1% y-o-y organic in Q4 (+4.3% in January-December) while churn remained stable.

Revenues totalled €12,400m in the fourth quarter (€48,422m in January-December) and decreased by 4.0% y-o-y due to the changes in the perimeter and the currency depreciation effect (-0.6% in January-December). In organic terms, revenues increased by 2.0% y-o-y in the fourth quarter (+3.2% in January-December), on the back of the sustained service revenue growth and handset sales.

OIBDA totalled €3,669m in October-December (€15,119m in January-December) and increased by 3.8% y-o-y (-2.9% in January-December) positively affected by the impact from IFRS 16 accounting standard adoption. It was negatively impacted in the quarter by the provisions for restructuring costs, the impacts of the transformation of the operating model of T. México after the agreement reached with AT&T, and the impairment of goodwill of T. Argentina.

In organic terms, OIBDA grew by 4.0% y-o-y in the quarter (+1.9% in 2019), on the back of revenue growth and savings (from digitalisation and simplification), among other cost control measures. Excluding extraordinary impacts, underlying OIBDA totalled €4,370m in the fourth quarter (€16,982m in January-December).

Net income totalled €986m in October-December (-€202 in reported terms) and reached €3,574m (€1,142m in reported terms), after excluding the following impacts, which totaled €2.432m:

- the deferred tax assets reversal of T. México (-€454m)

- the impacts of the transformation of the operating model of T. México (-€275m)

- the impairment of goodwill of T. Argentina (-€206m)

- the provisions for restructuring costs (-€1.614m)

- and capital gains and other factors (-€117m).

On the other hand, exchange rate evolution negatively affected the Company’s reported revenues for January-December 2019, mainly due to the depreciation of the Argentine peso against the Euro. This negative impact decreased significantly in terms of cash flow generation (-€173m).

Debt reduction for the 11th consecutive quarter

Net financial debt at December (€37,744m) decreased by €3,330m vs. December 2018 mainly driven by free cash flow generation, net financial divestments (€1,090m; sale of 10 Data Centers, T. Panamá, T. Nicaragua, T. Guatemala and Antares) and the issuance and replacement of capital instruments (€686m). In the fourth quarter, net financial debt decreased by €549m thanks to free cash flow generation (€1,762m).

In 2019, the financing activity of Telefónica amounted to €8,299m (without considering the refinancing of commercial paper and short-term bank loans) and focused on maintaining a solid liquidity position and refinancing and extending debt maturities (in an environment of low interest rates). As of the end of December, the Group has covered debt maturities for the next two years. The average debt life stood at 10.5 years (vs. 9.0 years in December 2018).

Telefonica’s digitalized network, a benchmark in efficiency

CapEx in January-December totalled €8,784m (+8.2% y-o-y) and included €1,501m of spectrum (€37m in Q4; €29m in T. Hispam Sur and €7m in T. España). It continued to focus on accelerating excellent connectivity (deployment of LTE and fibre networks, increased network capacity and virtualisation) and improving quality and customer experience (implementation of AI in the Company’s technology platforms).

OIBDA-CapEx reached €6,335m in January-December and grew +0.1% y-o-y organic (-15.0% reported). Free cash flow totalled €5,912m in January-December 2019 and increased by 20.6% y-o-y vs. 2018.

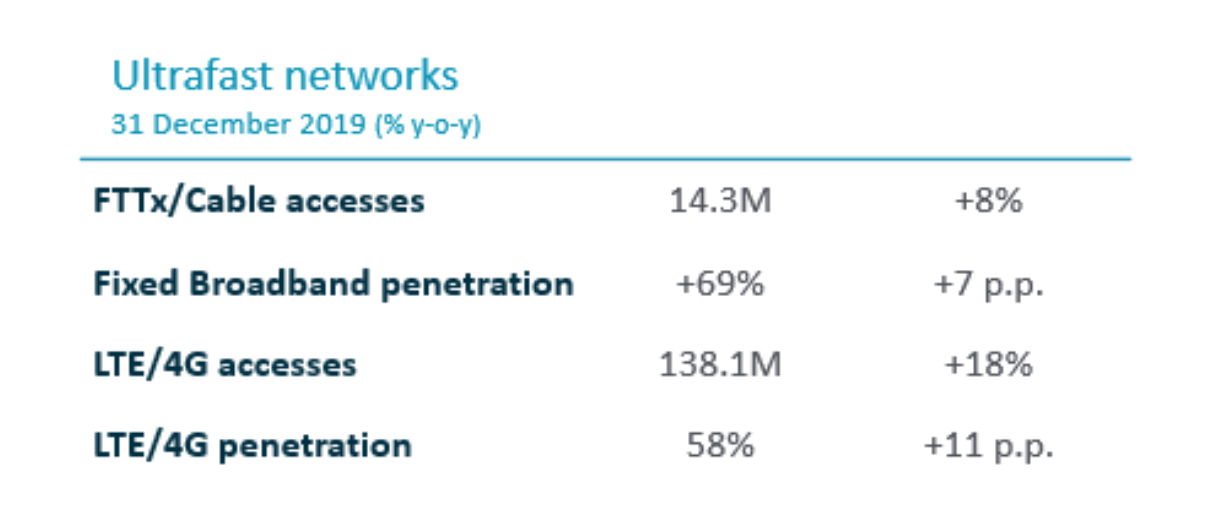

Telefónica continued evolving its network infrastructure and offering excellent connectivity, with Group’s FTTx/cable network totalled 127.8m premises passed. LTE coverage stood at 79%.

An acceleration of the E2E Digital Transformation programme helped capture more than €420m savings in 2019, above the target of >€340m, which are on top of the >€300m captured in 2018. Over two thirds of the €1Bn commitment of savings for the 2017-20 programme have already been achieved.

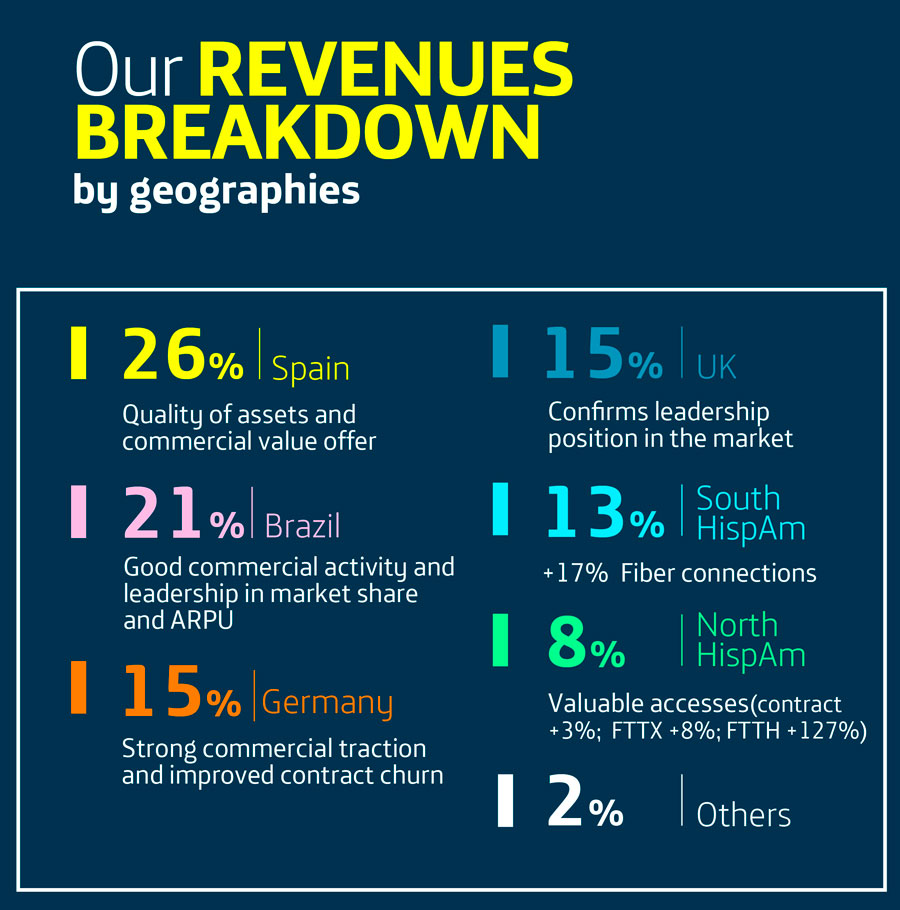

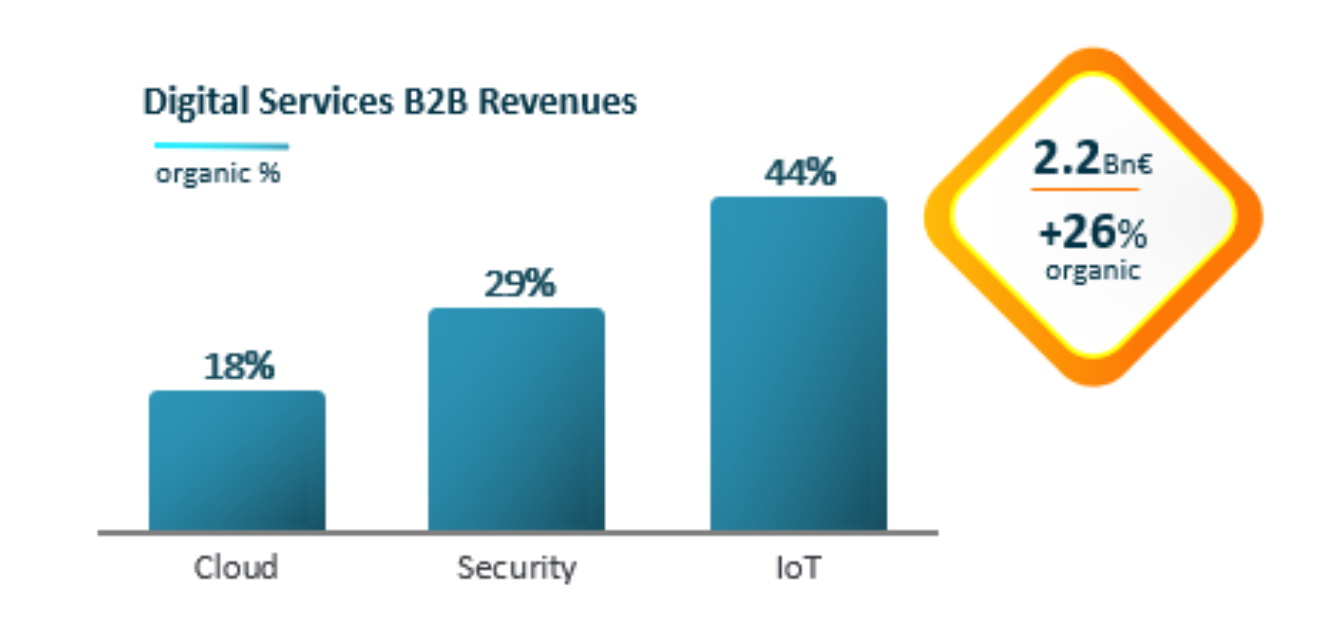

In the business segment, revenues in Q4 (€2,415m) were up 3.6% y-o-y and in 2019 (€9,458m) by 4.4% (Europe: €5,256m, +1.9% and Latin America: €4,201m, +7.2%) driven by digital services (€631m and +19.2% in Q4; €2,205m and +26.2% in 2019) mainly Cloud, IoT/Big Data and Security. The Group’s digital services revenue totalled €2,023m in Q4 (+11.5% y-o-y) and €7,745m in 2019 (+17.1%).

Definitions:

Organic growth: Assumes average constant foreign exchange rates of 2018, except for Venezuela (2018 and 2019 results converted at the closing synthetic exchange rate for each period) and excludes the hyperinflation adjustment in Argentina. Considers a constant perimeter of consolidation. Excludes the effect of the accounting change to IFRS 16, write-downs, capital gains/losses from the sale of companies, restructuring costs and material non-recurring impacts. CapEx excludes spectrum investments.

Underlying growth: Reported figures excluding write-downs, capital gains/losses from the sale of companies, restructuring costs, material non-recurring impacts and depreciation and amortisation charges from purchase price allocation processes.

Results by geographies:

(% organic y-o-y)

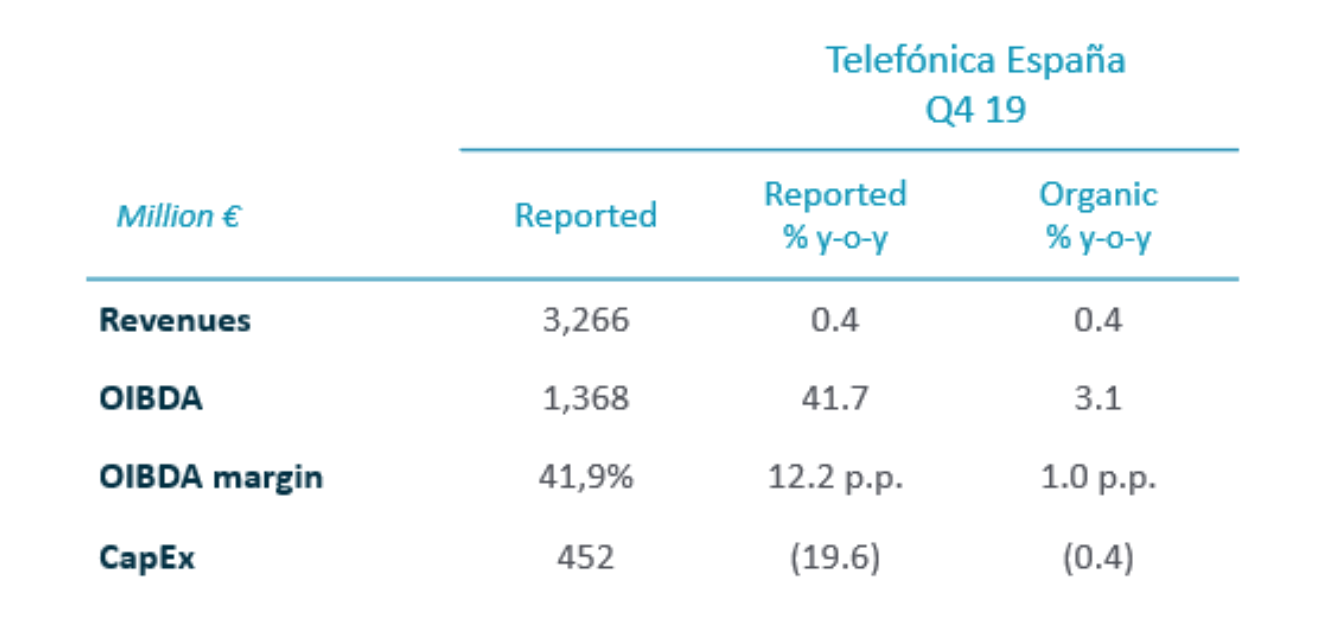

Telefónica España, revenue growth in all quarters. Telefónica España posted a y-o-y increase in service revenues in 2019, after growing in all quarters and in OIBDA. Convergent customers (4.7m) increased by 1% y-o-y and convergent ARPU stood at €88.4 in the quarter (+0.2% y-o-y).

Revenues in the quarter (€3,266m) rose 0.4% y-o-y, as did service revenues (handset revenues +1.5%). In 2019, total revenues (€12,767m) and service revenues (€12,394m) rose 0.5% and 0.6% y-o-y respectively. OIBDA growth accelerated significantly to +3.1% year-on-year in Q4 (€5,311m in underlying terms in 2019, €1,368m in the quarter), improving 2.9 p.p. vs. the previous quarter. In 2019 OIBDA grew 0,1% y-o-y. In organic terms, the OIBDA margin stood at 39.9% in Q4 (39.7% in 2019).

CapEx in January-December grew by 2.7% y-o-y due to the deployment of 4G and fibre networks, and OIBDA-CapEx in organic terms amounted to €3,423m (-1.2% y-o-y).

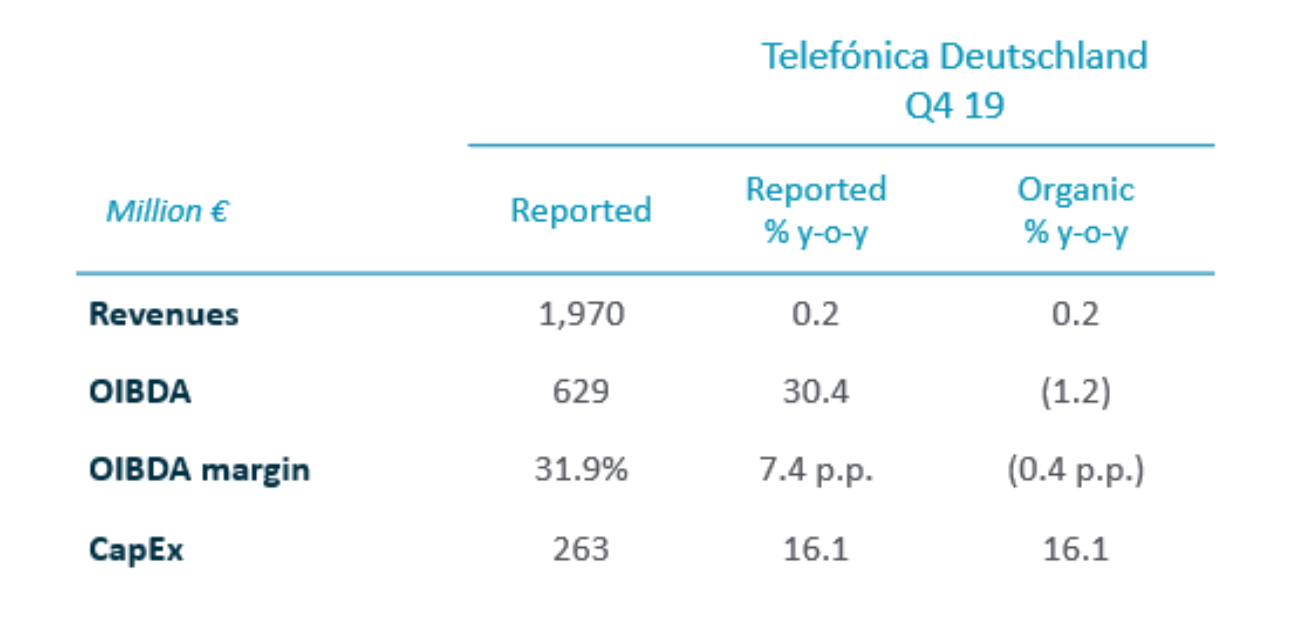

Telefónica Deutschland, growth in both customers and wholesale segments. Telefónica Deutschland posted a good set of operational results during the quarter and delivered healthy growth across both, own customers and wholesale partners. The ongoing traction of the O2 Free portfolio is satisfying the increasing customer demand for larger data bundles and supporting the company’s ARPU-up strategy.

Revenues increased by +0.2% y-o-y in Q4 19 and reached €1,970m (€7,399m in FY 19; +1.1% y-o-y). OIBDA reached €629m in Q4 19 and declined 1.2% y-o-y (€2,326m in FY 19; -1.1%) impacted by regulation (e.g. RLAH, intra-EU calling, MTR cuts) as well as the continued market investment into the positioning of the O2 brand. These impacts have been somewhat offset by the final integration synergies and early digital transformation savings. OIBDA margin stood at 31.9% in Q4, declining -0.4 p.p. y-o-y (31.4%; -0.6p.p. vs. 2018).

CapEx reached €2,469m in 2019 (including €1,425m of 5G spectrum obligations) and increased by 8.1% y-o-y, mainly due to 4G/LTE roll-out investments further enhancing customer experience. OIBDA-CapEx stood at -€143m in the period January to December 2019.

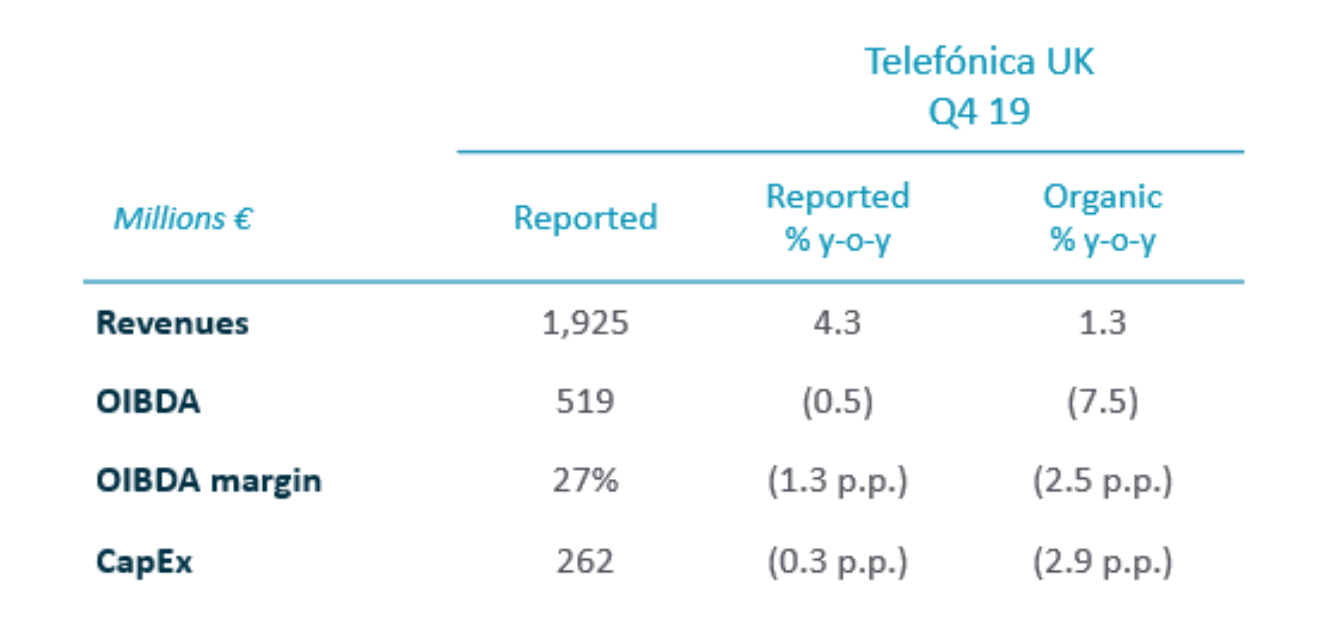

Telefónica UK, growth for the 14th consecutive quarter. Telefónica UK posted a 14th consecutive quarter of y-o-y top-line growth whilst also increasing customer base as it continued to deliver in a competitive market. Once again, the Company confirmed its market leading position and remained the UK’s favourite mobile network with a sector leading loyalty at 1.0%. These achievements are supported by the Company’s ongoing focus on championing customer fairness through product innovations such as flexible “Custom Plans”.

Revenues showed solid growth of 1.3% y-o-y to €1,925m in Q4 (€7,109m; +3.8% in FY 19). OIBDA fell by 7.5% y-o-y, totalling €519m in Q4 19 (+2.3% in FY 19; €2,114m), mainly due to higher ALFs and adverse y-o-y comparisons (positive non-recurrent factors of €29m in Q4 18). As a result, Q4 OIBDA margin stood at 27.0% (-2.5 p.p. y-o-y) and 29.7% in FY (-0.4 p.p. y-o-y).

CapEx increased by 3.4% y-o-y to €914m in FY 19, primarily as a result of investments in network capacity in 4/5G and customer experience. OIBDA-CapEx amounted to €1,200m growing by 1.4% y-o-y for the full year.

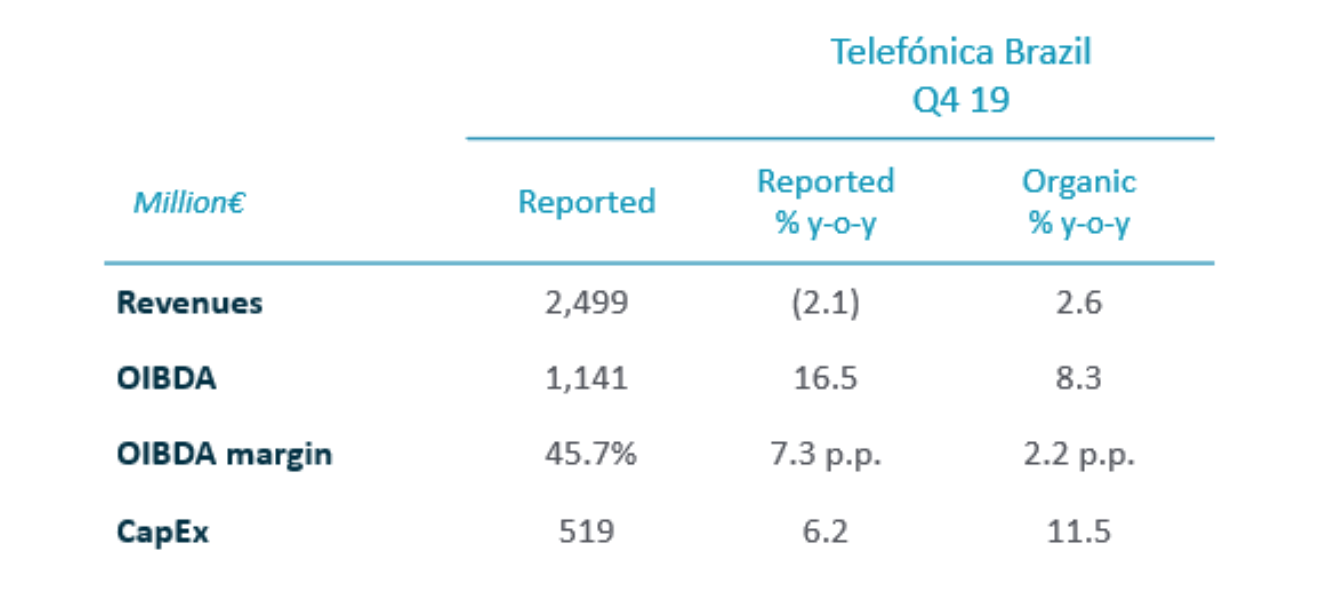

Telefónica Brasil, solid operating results and margin expansion. Telefónica Brasil ended 2019 with solid commercial and financial results; +8.3% y-o-y growth in OIBDA in the fourth quarter (+3.7% in the year) and 2.2 p.p. margin expansion (+0.7 p.p. in 2019) thanks to sustained revenue growth and savings mainly through digitalisation.

Operating revenues (€2,499m) maintained a solid y-o-y growth rate in Q4 (+2.6%, +1.9% in the year). OIBDA amounted to €1,141m in the quarter (+€107m due to IFRS16, +€431m in the year) and grew by +8.3% (+3.7% in the year), with a €29m positive impact related to the adequacy of international intellectual property. OIBDA margin stood at 45.7% in the quarter (+2.2 p.p. y-o-y) and at 42.5% in January-December (+0.7 p.p. y-o-y).

CapEx in January-December amounted to €2,005m (+7.9% y-o-y) mainly allocated for FTTH deployment (43 new cities deployed in the year) and the expansion of the 4G network to 3,206 cities (89% population coverage; +1 p.p. y-o-y). Thus, Capex accounted for 20% of revenues (+1 p.p. y-o-y). OIBDA-CapEx amounted to €2,257m in the year, decreasing 0.6% y-o-y as a result of the quicker pace of investments.

Telefónica Hispam South, positive contract accesses evolution. Hispam South posted solid y-o-y growth in revenues and OIBDA driven by the positive performance of contract and FTTx/cable accesses, tariff upgrades in Argentina and efficiency savings, which more than offset the macroeconomic situation and competitive environment in the region (mainly in Chile and Peru).

Revenue for Q4 totalled €1,599m, +11.9% y-o-y (+15.3% in 2019), sustained by Argentina and by the overall growth in contract and fibre revenues in the region, despite negative regulatory impacts in Chile and Peru (-1.5 p.p. to the quarter’s growth, -1.8 p.p. in 2019). OIBDA (€131m in Q4; +€43m due to IFRS 16 and +€123m in 2019) grew 9.3% y-o-y in the quarter (+12.6% in 2019). Q4 OIBDA was impacted by -€206m associated with the impairment of goodwill allocated to T. Argentina. OIBDA margin stood at 8.2% (-0.6 p.p. y-o-y) and at 21.9% in January-December (-0.6 p.p. y-o-y).

CapEx in FY 19 totalled €965m (including €6m for spectrum in Argentina and €26m in Uruguay, mainly booked in Q4) and rose 0.2% y-o-y associated with the deployment of 4G and FTTx and cable network. Capex accounted for 15% of revenues (-2 p.p. y-o-y). OIBDA-CapEx amounted to €433m in FY 19 (+32.0% y-o-y).

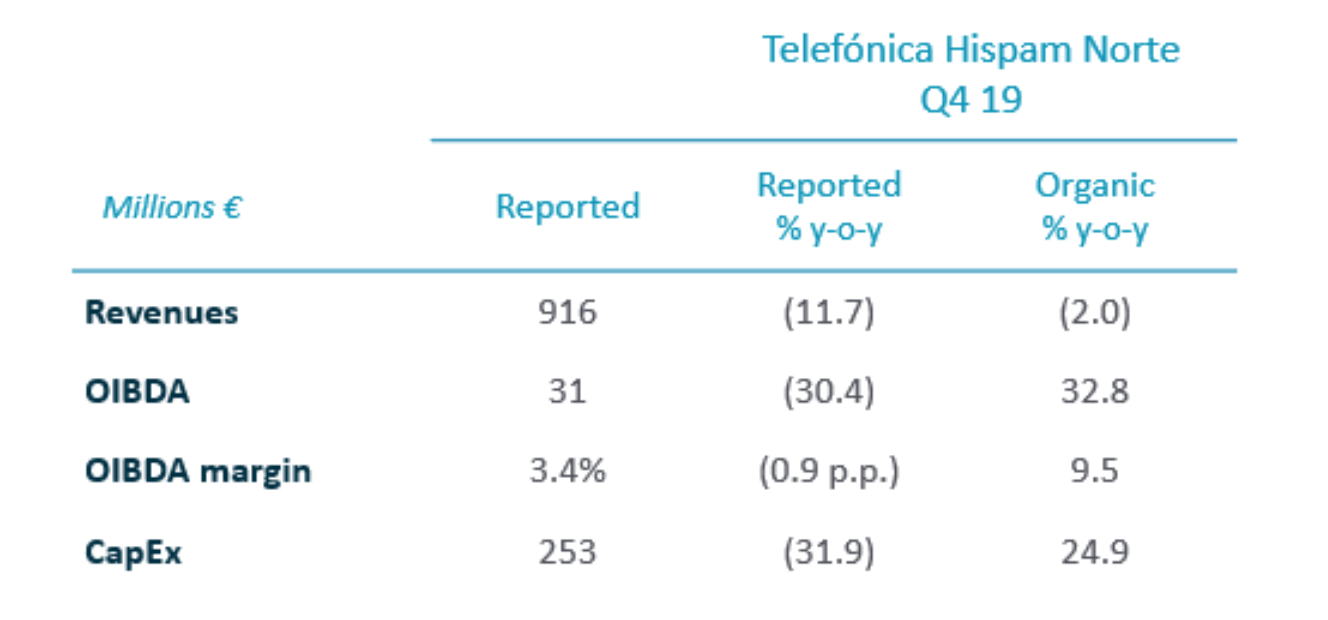

Telefónica Hispam North, focus on value customers. In the fourth quarter of 2019, Hispam Norte OIBDA was positively affected by €99m capital gains from the sale of towers in Colombia and Ecuador, as part of the strategy to maximise the value of the group’s infrastructure. Furthermore, the company remained focused on value accesses (FTTx +8%, FTTH +127%, contract +3%), worth highlighting another quarter with positive contract net adds in Colombia and Mexico.

Revenues (€916m) fell 2.0% y-o-y in the quarter (€3,795m, -0.8% in FY 19), affected by Ecuador’s macroeconomic environment, although it is worth mentioning the growth acceleration in Mexico (+1.7% y-o-y in Q4; +0.5% in FY 19) and the return to positive growth in Colombia (+0.2% in Q4; +1.1% in FY 19). OIBDA (€31m; -€22m due to IFRS 16 adoption; +€94m in FY 19) increased 32.8% y-o-y in the quarter (€830m in FY 19, -3.1%). In the quarter, OIBDA was impacted by -€239m, as a consequence of the operational model transformation following the agreement with AT&T.

CapEx (€580m in January-December) increased 11.6% y-o-y mainly due to investments related to a contract awarded by the Colombian Government for the digital transformation of its institutions (€74m in Q4). €38m for spectrum renewal mainly in El Salvador (Q1 19) and in Mexico (Q3 19) were registered in FY 19. CapEx represented 14% of revenues in FY 19 (+2 p.p. y-o-y). OIBDA-CapEx totalled €251m in FY 19.

Related documentation

Shareholders and Investors Section

Here you have data about the conference call, in which the most significant aspects of the results are commented.

Other news of interest