In July, we launched the series entitled EC White Paper , where we present Telefónica’s contribution to the public consultation on the White Paper. As a result of this consultation, the Commission will present a legislative proposal, the Digital Networks Act , which will determine the future of the European Union and the telecommunications sector in the next decade through a new regulatory framework.

The first post looked at the proposed future for the telco sector, the second post looked at the new challenges facing the new Commission. The third addressed the Internet imbalance and in this fourth post we look at the issue of access regulation.

Does the current model of ex ante regulation support the achievement of the objectives of the Digital Decade by 2030?

There has been much debate over the past year on the EU’s strategic strategic autonomy of the EU and about the delay in the deployment of VHCN (Very High Connectivity Networks) in Europe compared to other geographies such as China or North America. In this context, it is becoming increasingly important to identify and implement policies and regulatory frameworks that will provide incentives for investment in the sector and help to reduce the investment gap of around 200 billion euros that the EC has estimated would be necessary in order to achieve the objectives set by the EC in its DD (Digital Decade) 2030.

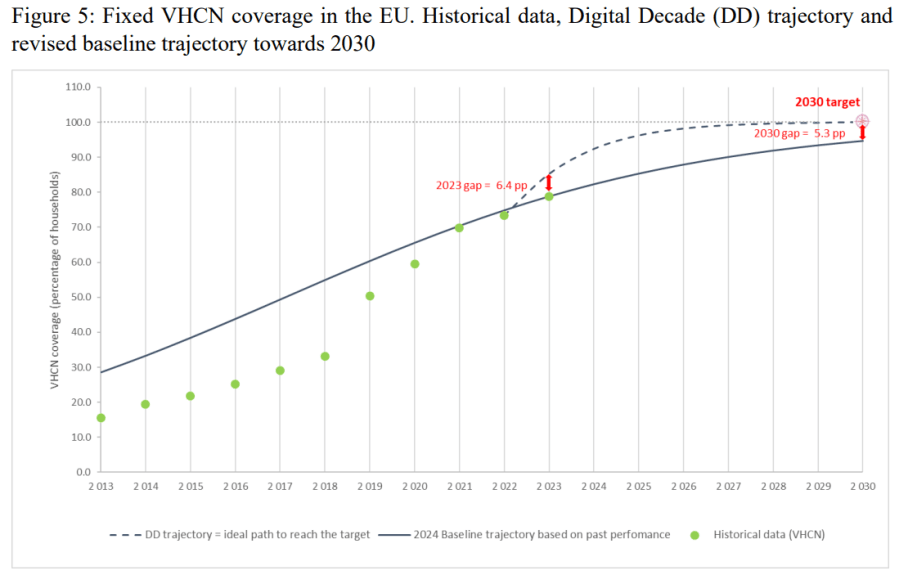

Thus, if the current pace of investment in the sector in Europe is maintained, 5.3 percentage points would be short to meet the target of 100% coverage of European households with gigabit fixed broadband (VHCN), according to the latest EC report on “The State of the Digital Decade” published in July 2024.

In the case of the coverage target for FTTP networks (Fibre to the premises), this gap would double to 10.5 percentage points. These data show a material delay against the target and are a clear example that the sector needs policies that encourage investment to deploy this type of networks.

What proposals would improve incentives for investment in the sector?

The problem between the sector’s investment incentives and the regulatory framework has been analysed within the White Paper (WP) published by the EC in February 2024. In it, it proposes as an alternative to boost the deployment of this type of networks, the elimination of the current fibre wholesale markets (M1 and M2), with only the civil infrastructure market being subject to ex ante obligations, together with the price flexibility set out in the Gigabit Recommendation.

In our opinion, this proposal should be much more ambitious in order to be able to undertake with guarantees the reduction of the investment gap since, despite the elimination of relevant markets, regulators would have the possibility to intervene in the markets with the application of the 3 criteria and could therefore analyse possible competition problems in a very similar way as they do now (identification of SMP operators and imposition of ex ante obligations).

A practical example of how the approach proposed in the WP would not bring about a material change to the current approach and would not provide the necessary investment incentives is what happened with the market 3b for fiber wholesale access in Spain.

This market was removed from the list of Relevant Markets by the EC in 2020 and, however, in the market analysis carried out by the CNMC in 2021, the need for this market to continue to be regulated was determined, despite the active competition at wholesale fibre level that existed at that time between the different operators. Therefore, despite the proposed simplification of the list of relevant markets, regulators would still retain the possibility to intervene ex ante in the markets and therefore the current competitive dynamics would continue, but more importantly, without significant changes in regulatory certainty and investment incentives for operators.

Towards a new regulatory approach to the telecommunications sector

In the recent Draghi report, which addresses how to boost the competitiveness of European industry in particular, makes it clear that the fragmentation that the European Telco sector has suffered over the last decade has been the result of the application of an artificial regulatory and competition policy that has in no way encouraged investment by operators.

The report makes a firm commitment on how regulation in the Telco sector should be oriented, abandoning ex-ante regulation at national level as it discourages investment and increases risks.

Instead, it proposes the application of an ex-post policy (current competition law) for cases where an abuse of dominant position or any other anti-competitive behaviour is identified. In this regard, the Spanish market, given the significant fibre deployments by a multitude of players, should undoubtedly be a pioneer in this change of approach and regulatory model.

On this basis and in line with the Draghi report, the current regulatory model based on the analysis of relevant markets and the identification of an SMP operator on which ex ante obligations fall, neither facilitates the creation of an ecosystem where sustainable infrastructure competition can develop nor favours the incentive for private investment for the deployment of fibre networks.

From ex-ante regulation to a competitive model based on the right to competition

This calls for a profound change in the approach to the regulated model of access to fibre networks. If private investment in fibre networks is really to be incentivised to accelerate its deployment, it is necessary to abandon the current ex ante regulation and migrate to a model in which the application of competition law (ex post) complemented by an efficient application of the horizontal framework that the Gigabit Infrastructure Act (GIA) provides to guarantee access to civil infrastructure, would be sufficient to ensure retail competition in the sector.

Only when certain conditions exist in the wholesale market that allow the presence of a bottleneck to be enduring over time or the conditions are not right for forward-looking infrastructure competition, regulatory intervention could be envisaged.

In this sense, the presence of an active competitive supply of fibre at wholesale level would ensure competitiveness at retail level, and ex ante obligations in that geography could be removed. Where there is an active competitive wholesale offer, allowing third parties to compete at the retail level with a national offer, ex ante obligations should be abandoned, and the market should be governed solely by the application of competition law and the GIA.

In those geographies where third parties cannot access an active competitive wholesale offer and where the GIA does not guarantee infrastructure competition, regulatory intervention would be envisaged and should focus on the imposition of a competitive wholesale offer by the operator managing the network bottleneck.

In the next post we will delve deeper into whether the regulatory model limits innovation in the telecommunications sector.