Connect Europe has recently published its third consecutive annual report on the State of Digital Communications in Europe (2025), providing a comprehensive analysis of the sector’s competitiveness and the key trends shaping its future.

This year’s edition is particularly important as it serves as a starting point for advancing the reforms needed to improve Europe’s digital and technological capabilities to boost productivity and close the innovation gap, an urgency widely highlighted in the Draghi and Letta 2024 reports. 2025 is the year for action. Where does Europe stand in the global digital landscape, what is at stake and what reforms are needed to strengthen its competitiveness?

The strategic relevance of the telecom sector into figures

In its 2025 State of Digital Communications report, Connect Europe put into figures the strategic importance of the digital sector recognized by Draghi and Letta: the market, including telecom services, network equipment, and content & applications, was valued at EUR 1 trillion in 2023, or 4.7% of Europe’s GDP. For comparison, agriculture, fisheries, and forestry collectively contribute 1.7% to GDP.

Connect Europe emphasizes that the telecoms sector is a key pillar of the connectivity ecosystem, driving prosperity. Total investment in the market amounted to 115.5 billion euros, with telecommunications operators leading the way, accounting for 60% of the total, followed by content and application providers (just over 30%) and equipment manufacturers (almost 10%).

This investment, particularly, in fixed and mobile networks enables technological progress and cutting-edge digital experiences and services, as well as transformative technologies like 5G, AI, IoT, and cloud. In addition, the sector ensures the interconnection of technologies, devices and players, sustaining the seamless functioning of the digital ecosystem, key for innovation.

The report also presents figures on the potential impact of AI on data traffic, with the most significant effects observed in data centers, where AI-related traffic volumes are expected to grow at a CAGR of 50% or more. Operators will need to support this surge. Additionally, the report includes data on cybersecurity retail revenues, which are projected to increase by over 9% due to the growing role of operators in cyber protection and the increased demand.

Considering the sector’s strategic value and trends, Connect Europe emphasizes that 2025 is likely to be a “now-or-never” moment for Europe, if it is to stay in control of its connectivity value chain and drive growth.

The current State of Digital Communications in Europe

The urgency of the moment stems from Connect Europe’s telecom sector “competitiveness health check”. It is first worth to note that this sector is highly capital-intensive, requiring substantial investment in infrastructure, networks, technology, and R&D. To remain viable and competitive, operators must achieve sufficient scale, particularly in terms of revenue and profitability, to sustain ongoing investment and innovation.

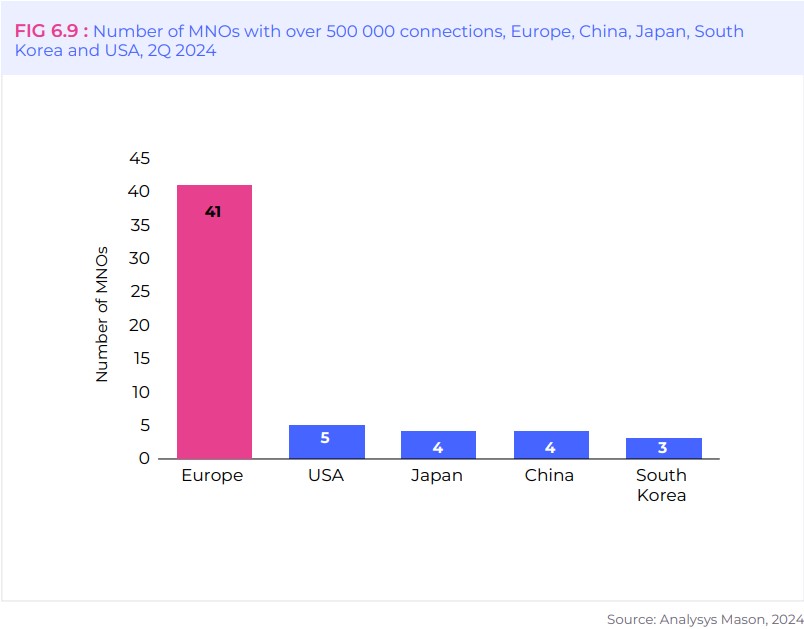

However, Connect Europe’s main conclusion is that an overly fragmented market (41 mobile network operators with over 500,000 connections in Europe, compared to 5 in the USA or 4 in China o Japan), burdened by heavy rules and lack of scalability, is seeing a halt in investment growth for the first time in years.

The continuation of unhealthy trends in revenues and return on capital underscores the urgent need for policy and regulatory reforms. Connect Europe refers to Draghi’s report to note that European telecoms Return On Investment (ROCE) is declining since 2017 (5.9% in 2023 vs. 6.6% in 2017) and it even stands below the cost of capital, discouraging investments.

Consequences of current trends for Europe’s competitiveness and the welfare of its citizens

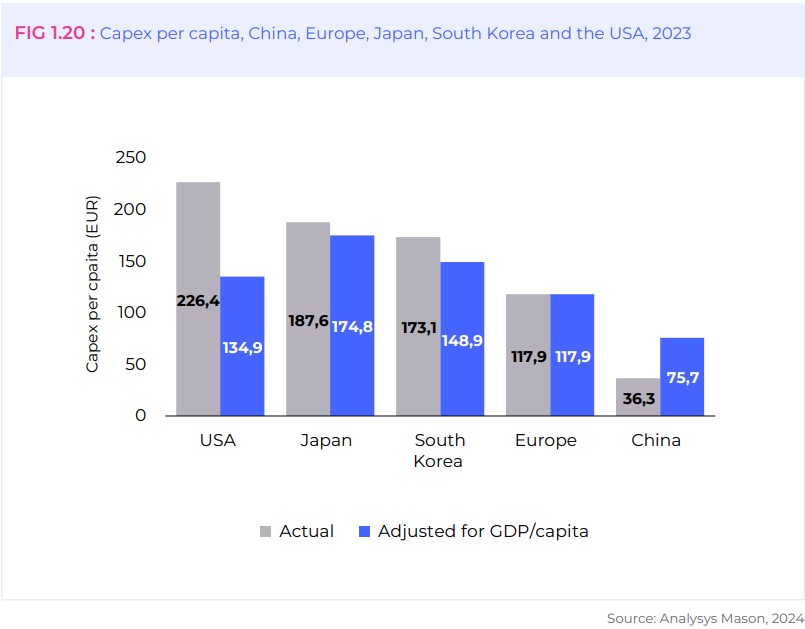

Despite the significant investment efforts of European telecom operators—estimated by Connect Europe at approximately EUR 58 billion in 2023—this level of investment still falls short of ensuring the necessary per capita funding to provide European businesses and citizens with access to services of the same or higher quality as those available in other regions, putting at risk competitiveness and welfare.

In fact, Europe’s telecom investment per capita in 2023 (EUR117.9) is almost half that of the USA (EUR226.4) and below other regions.

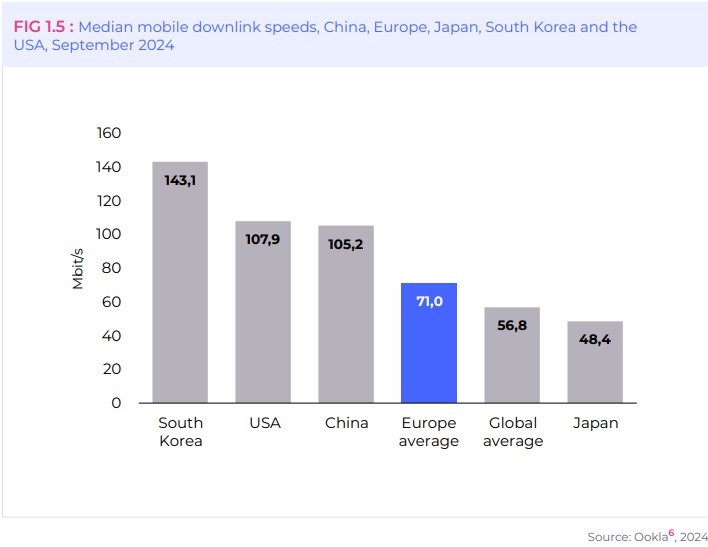

As a consequence, according to Connect Europe, Europe has lower network performance. In concrete, download speeds in Europe are 44% lower for fixed networks (137 Mbit/s in Europe vs 246 Mbit/s in USA) and 33% lower for mobile networks compared to the USA (71 Mbit/s in Europe vs 107.9 Mbit/s in USA).

In addition, the EU Commission’s latest report on the State of the Digital Decade highlights that the 2030 goals of 100% gigabit and 5G population coverage are still far from being met and current progress indicates that Europe is falling behind its global peers and falling short of the Digital Decade Targets.

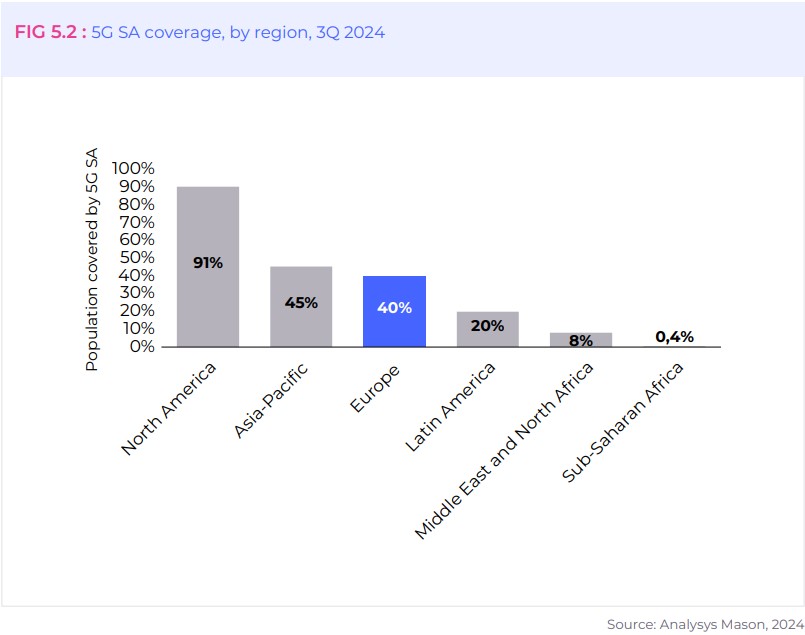

An example is the progress of 5G standalone (SA) roll-out. As a cornerstone of digital transformation, 5G SA enables ultra-low latency, higher reliability, and greater efficiency. Its key feature, network slicing, allows operators to create tailored virtual networks for industries, powering innovations like autonomous vehicles, smart factories, or remote healthcare. However, 5G Standalone (SA) coverage reaches only 40% of the European population, far behind North America’s 91%.

As a result, delays in building the digital infrastructure needed for future demands and technologies put at risk European consumer welfare, innovation, competitiveness, and scalability in the long term.

Which policy reforms would reinforce the sector competitiveness?

In this context, Europe needs to prioritize the telecoms sector competitiveness by implementing the necessary measures that encourage investment and innovation.

The inclusion of the Digital Networks Act (DNA) in the Commission’s 2025 Work Programme is therefore a positive step. It presents a crucial opportunity to tackle Europe’s digital infrastructure challenges, foster an investment-friendly environment, and ensure the long-term sustainability of the region’s digital connectivity value chain.